November 29, 2021

Washington’s Struggles with Inflation

On November 10, the Labor Department reported that inflation rose by 6.2% over the past year, the largest yearly increase in 30 years. In response to the 2008-2009 financial crisis and the COVID pandemic, Washington produced an unprecedented expansion in fiscal and monetary policy. The federal debt has more than tripled, and the Fed has lowered interest rates to near zero and increased its balance sheet nearly 10-fold. Instead of igniting inflation, the Fed’s challenge has been to support a weakened economy and avoid deflation with low interest rates. That has changed.

A week before the inflation report, the Fed indicated that inflation was a rising concern and announced that it would begin to “taper” its quantitative easing program. The Fed still concludes that inflation is “transitory,” resulting from supply chain problems, and will dissipate as the economy recovers. But many economists believe the Fed is moving too slowly, is “behind the curve” in combatting the problem, and inflation is getting embedded in the economy. With the November inflation report, President Biden expressed his concerns about inflation.

We have to be aware of the risks… particularly now the risk of significantly higher inflation.

Federal Reserve Chairman Powell,

November 3

In our April report, we wrote about the risks rising interest rates pose to the Federal budget. While we correctly forecast the risk of interest rates higher than the Congressional Budget Office’s (CBO) February projection, economic growth has been stronger, and higher revenues more than offset the additional cost of higher interest rates. The economy, however, is unlikely to continue to grow at the pace it has over the past year. If inflation persists and interest rates rise as economic growth moderates, the federal budget’s bottom line will be hit.

In April, we looked only at the impact of interest rate changes. Although higher inflation increases Federal spending, it also increases federal revenue so higher inflation has little net impact on deficit projections. However, CBO assumes that higher inflation is accompanied by higher interest rates, causing large net increases in the deficit. The combination of higher inflation and interest rates, and their impact on the federal budget, should be a factor in federal contractors’ long-term planning.

And, on inflation, today’s report shows an increase over last month. Inflation hurts Americans’ pocketbooks, and reversing this trend is a top priority for me.

President Biden,

November 10

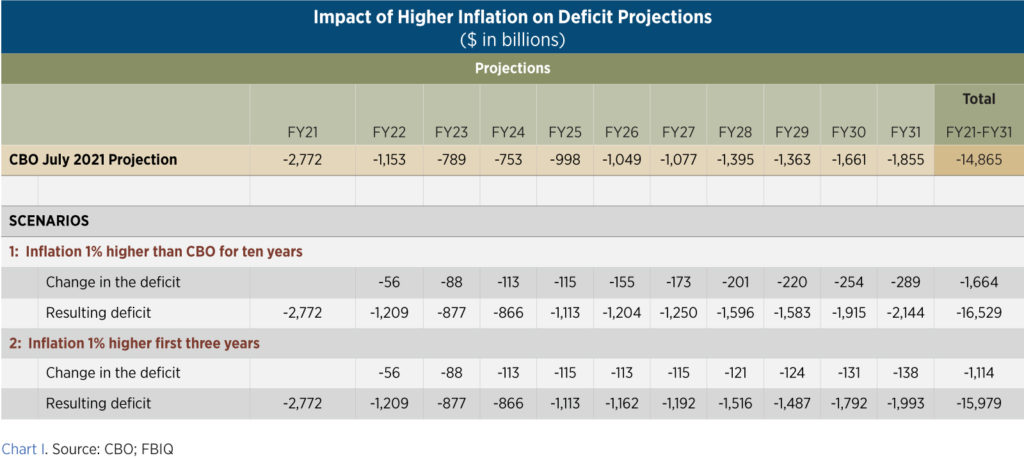

Chart I takes the deficit projections in CBO’s July budget forecast and illustrates the impact of two scenarios. The first, an embedded inflation scenario, adds one percentage point to the inflation rate to CBO’s July forecast, taking inflation up to a little over 3% for the next ten years. The second, a transitory scenario, assumes inflation is one percentage point higher than CBO’s July forecast for three years and then returns to CBO’s July forecast of a little over 2% for the subsequent seven years. The first scenario results in an estimated $1.7 trillion increase in deficits over the next ten years and the second scenario results in a $1.1 billion increase in the deficit over that period.

The federal budget is highly sensitive to the economy where small swings in economic variables lead to very large swings in deficits and debt. As a result, if higher inflation and interest rates are temporary and accompanied by stronger economic growth, that is likely to offset higher deficits and may even improve the fiscal picture.

While higher inflation and interest rates represent a possible threat to the budget, the public is much more concerned about its impact on their pocketbooks. With gasoline, food, and other prices rising rapidly, congressional Republicans’ argument that inflation is being driven by Democratic fiscal policies appears to be gaining traction with the public. As a result, inflation poses both a deficit risk to the budget and a risk that policy makers will address the public’s ire by constraining federal spending that has largely been unrestrained for the past five years. For public sector contractors, this translates to a funding risk for their agency customers whose programs may face more budget limitations.