On March 15, 2022, the Federal Reserve began raising interest rates from essentially zero to a peak level of between 5.25% and 5.5% on July 26, 2023. With the steep rise in interest rates, many economists in 2022 and 2023 were predicting the U.S. was headed into a recession. They were wrong. Unemployment remained low, the economy continued to grow, inflation declined, and the stock market soared, increasing 45% through September 15, 2025.

In support of our goals and in light of the shift in the balance of risks, today the Federal Open Market Committee decided to lower our policy interest rate by a quarter percentage point.

Federal Reserve Chairman Powell,

September 17

IS THE ECONOMY STALLING?

Economic data thus far in 2025 includes mixed signals suggesting that the economy may be weakening. On September 9, the Bureau of Labor Statistics (BLS) released a 911,000 downward revision to its estimate of job growth from March 2024 to March 2025. For August 2025, BLS reported job gains of only 22,000 for the month. The New York Federal Reserve Bank’s August consumer expectations survey reported that employees felt that if they lost their job that the chance of finding a new job was 44.9%, the lowest level reported since the survey began in 2013.

In addition to a slowdown in job growth, the Trump administration’s aggressive immigration enforcement actions have decreased the supply of labor. The home construction market continues to be depressed, and the Trump Administration’s tariff increases are expected to weaken economic growth and cause a temporary increase in inflation.

The Federal Reserve is struggling to strike a balance between its dual mandate of maximizing employment while keeping inflation under control. While inflation has declined significantly from its 2022 peak levels, inflation still remains at about 3%, well above the Federal Reserve’s 2% target. Due to its concern about the labor market, however, the Federal Reserve reduced the federal funds rate by 25 basis points to a range of 4.0 to 4.25% on September 17th, and signaled a two more possible reductions of 25 basis points at each of its two remaining meetings for the year.

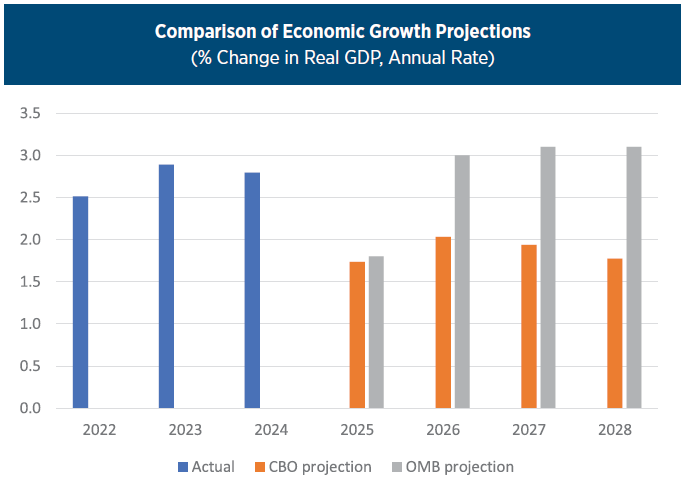

Chart I. Source: OMB, CBO, FBIQ

A RESILIENT ECONOMY?

In the face of a weakening labor market, a boost in tariffs not seen since the 1930s, and interest rates that have risen to levels that have not been experienced for nearly two decades, the U.S. economy remains remarkably resilient. It continues to generate real economic growth (real GDP grew by 3.3% annual rate in the second quarter of 2025), at 4.3% the unemployment rate remains at historically low levels, and the dynamic and resilient nature of the U.S. economy combined with an artificial intelligence boom may be generating sustained productivity gains (productivity increased 3.3% in the second quarter of 2025). The Trump administration also is actively reducing regulatory burdens on the economy to spur economic growth. Finally, the economy is likely to get a significant boost from the reconciliation law, when an estimated $277 billion in economic stimulus from net additional spending increases and new tax incentives for businesses and individuals ramp-up in 2026.

We are going to push through with the economic policies that are going to set the economy right. I believe by the fourth quarter we are going to see a substantial acceleration.

Treasury Secretary Bessent,

September 7

TWO DIVERGING VIEWS OF THE ECONOMIC OUTLOOK

On September 5, the Office of Management and Budget (OMB) released the “Mid-Session Review” to the FY26 budget, which included the Administration’s economic forecast for calendar years 2025-2035. A week later, the Congressional Budget Office (CBO) updated its economic projections for calendar years 2025-2028 (CBO plans to update both its 10 year budget and economic projections early next year).

OMB’s economic forecast assumes all the President’s policies will be implemented whereas CBO’s forecast is based on current laws. The two forecasts are remarkably different in their view of the economic outlook. Neither project a recession and both assume an economic boost in 2026 from the reconciliation law. The Trump Administration projects a strengthening economy with declining unemployment, inflation, and interest rates. CBO has a much more cautious outlook. The Fed’s September forecast is similar to CBO’s forecast.

The most significant differences in the agencies’ two forecasts are their projections of economic growth. The Administration projects real GDP growth of 3.2% in 2026 and real growth continuing at a 3.1% rate for each of the next two years. CBO assumes real economic growth rises to 2.0% in 2026 that slows to 1.8% by 2028. CBO concludes that while the reconciliation law boosts growth over the short run, that growth is partially offset by the effects of lower supply of labor primarily due to immigration enforcement and the net negative impact of tariffs (lower economic growth and a temporary rise in inflation). In nominal dollars over the four-year period, OMB projects the economy will grow by $2.5 trillion more than CBO.

The economy has a huge impact on the fiscal outlook. OMB’s Mid-Session Review projects the reconciliation law combined with other Trump Administration policies will boost economic growth and reduce the deficit $5.6 trillion over 10 years. That seems highly unlikely. Most economists expect the economy to slow but avoid a recession. In addition to the fiscal impact, the electorate tends to vote its pocketbook and the economy is likely to be a key factor in the outcome of the 2026 mid-terms.