February 22, 2022

State and Local Fiscal Recovery Fund is All Systems Go

Spring will bring two major milestones for the $350 billion Coronavirus State and Local Fiscal Recovery Fund (SLFRF), which was enacted in the American Rescue Plan Act (P.L. 117-2).

First, on April 1, 2022, the Final Rule covering the entirety of the SLFRF (eligible use, administration, reporting) will be in effect. The Department of the Treasury announced the Rule in early January and published it in the Federal Register on January 27, describing the changes to the Rule as delivering “broader flexibility and greater simplicity” for recipients.

Second, in May, counties, localities, and 30 states will receive the second half of their Fund payments—totaling $104.6 billion. Twenty states, including California, New York, and Texas, received all funding in one payment in May 2021 due to higher unemployment levels. Tribes and territories also received their full funding in 2021.

The Final Rule has been received positively by states and localities seeking flexibility and certainty. The SLFRF has been operating under an interim rule since May 2021. As part of the rulemaking process, Treasury solicited comments from stakeholders over the summer, receiving over 1,500 replies. The Final Rule addresses those by highlighting pertinent questions by topic and providing Treasury’s response. Treasury highlights several changes in the Final Rule including: 1) broadening eligible uses, including capital expenditures; 2) greater flexibility in eligible broadband investments with a focus on access, affordability, and reliability; 3) easier use of premium pay; and 4) simplification of administrative, reporting, and compliance requirements.

A quick recap of the SLFRF statute helps to frame the funding decisions ahead for states and localities. Spending is allowed in four separate eligible use categories, without target levels or caps: 1) replace lost public sector revenue—this means that SLTTs may use funds to provide government services up to the amount of revenue lost due to the pandemic; 2) respond to public health and negative economic impacts of the pandemic; 3) provide premium pay for essential workers; and 4) improve water, sewer, and broadband infrastructure.

The most impactful simplification of the Fund’s administrative requirements is related to revenue loss. Treasury cuts red tape and allows up to a $10 million revenue loss allowance to be taken as a standard deduction (rather than requiring a complex full revenue loss calculation method). The National Association of Counties estimates that 70% of counties will be able to use the simple deduction to cover their revenue loss. This means that funds will be available to localities more quickly and may be used in the most flexible ways. In essence, funds can be used to deliver government services for any purpose that does not violate SLFRF rules.

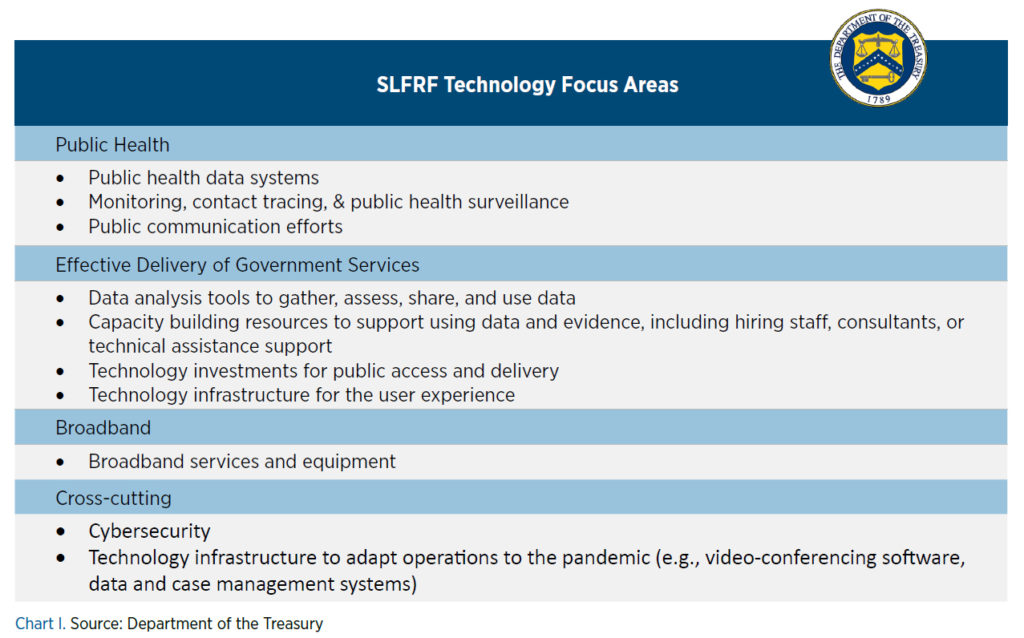

Technology uses—from system and equipment purchases to analytical support and cybersecurity investments—are expressly allowed. As seen in Chart I, the Final Rule specifies many eligible uses for information technology and analytical support, (many in response to questions raised during the rulemaking process), but Treasury stresses that the list is illustrative and not exhaustive. More information is available in Treasury’s overview of the Final Rule.

The final rule also clarifies and adds some restrictions on use of SLFRF resources. SLFRF funds must be obligated by December 31, 2024, and expended by December 31, 2026. As set in the statute, restrictions on SLFRF use include reducing taxes, deposits into pension funds, debt service and replenishing reserves, and settlements and judgments. The Final Rule prohibits “a term or condition that undermines efforts to stop the spread of COVID–19,” any violation of conflict-of-interest requirements, and waiving environmental requirements. In some cases, rules differ depending on recipient, such as for Tribes. See Treasury’s Compliance and Reporting Guide for specifics.

States will also be working on digital infrastructure plans as part of the $10 billion Coronavirus Capital Projects Fund, which was included in the American Rescue Plan Act. The purpose is “to carry out critical capital projects directly enabling work, education, and health monitoring, including remote options, in response to the public health emergency.” Allowed infrastructure projects include Broadband, Digital Connectivity Technology (focused on equipment), and Multi-Purpose Community Facility Projects. Treasury guidance notes that other projects may be considered. Each state, Tribe and territory has a preliminary allocation of funds, with a deadline to submit grant plans for Coronavirus Capital Projects by September 24 for the Treasury approval process. On January 4, Treasury posted updated FAQs for the program, which addresses, for example, questions regarding middle-mile or last-mile focused projects.

Even with this flexible funding windfall, states and localities face challenges. Making investments that help to manage future costs, such as renewing IT infrastructure and equipment, will help localities deal with the drop-off of federal funding. From governors to local councils, the balancing act of funding immediate needs versus longer-term ones is evident. On the political side, which investments are most needed, what do voters want to see, and which projects may be eligible for other funding such as from the Infrastructure Investment and Jobs Act?

For state and local governments with a depleted workforce and outdated IT infrastructure, administering these new funds will be a struggle. Using SLFRF funds to staff up and buy IT systems and infrastructure to support effective program management (and comply with federal law) might be the wisest start to 2022.