On May 16, President Biden met again with the four congressional leaders —Speaker McCarthy (R-CA), House Democratic Leader Jeffries (D-NY), Senate Majority Leader Schumer (D-NY), and Senate Republican Leader McConnell (R-KY). After the session, the president and congressional leaders agreed to pursue a bipartisan deal that could pass both houses of Congress to avoid a default. They also agreed that the President would designate individuals to negotiate directly with McCarthy’s team.

I will do everything in my power to avoid it [a default].

President Biden,

May 9, 2023

The Speaker gave extended remarks after the meeting at the White House and again at the Capitol. The White House issued a readout of the meeting that was much more subdued than his May 9 remarks. President Biden departed for Japan on Wednesday to attend a G-7 meeting but decided to cut his international trip short in order to return to Washington on Sunday.

Since May 9, staff from the White House and the four leaders’ offices have met regularly and made some progress in identifying potential areas for compromise but those meetings became unwieldy, particularly with time running out on Treasury’s borrowing authority. Agreeing to “shrink the room” for future negotiations to representatives from the White House and the Speaker’s office increases prospects for agreement. The President will be represented by Steve Ricchetti, a White House counselor who has developed a working relationship with congressional Republicans and OMB Director Shalanda Young. McCarthy will be represented by Rep. Garrett Graves (R-LA), a McCarthy confidant who helped him navigate his way to the Speaker’s gavel, along with representatives of McCarthy’s staff.

The President agreed to appoint a couple people from his administration to sit down and negotiate directly with my team so I found that to be productive, but we’ve got a lot of work to do in a short amount of time.

Speaker McCarthy (R-CA),

May 16, 2023

Although a default cannot be completely ruled out, we think it is unlikely. Instead, we think the President and congressional leaders will reach a budget agreement that sets caps for at least two years, includes other budget savings and reforms, and raises or suspends the debt limit past next year’s election.

THE AMORPHOUS DEBT LIMIT DEADLINE: THE “X DATE”

Congress has a difficult time passing controversial must-do legislation and frequently waits until the last minute to act. Unlike the deadline for government funding, which is October 1st of each year, the exact date Treasury will exhaust its borrowing authority and default, known as the “X date,” is hard to pin down. The Treasury processes millions of transactions in the form of receipts and disbursements of funds. Since it does not control the exact timing of those transactions, it is impossible to predict the exact X date well in advance.

On May 15, Treasury Secretary Yellen wrote congressional leaders reiterating her May 1 warning that if the debt limit was not raised Treasury could default as early as June 1. Since then, other projections have been along the same lines. On May 12, CBO warned “there is a significant risk” that Treasury will be unable to pay all its obligations sometime during the first two weeks of June. If Treasury has sufficient balances to get to June 15th, when quarterly estimated tax payments are due, the resulting revenue surge along with other factors will probably allow it to get to early August before the X date is hit.

If Treasury confronted a default, based on a 2011 Federal Reserve Board conference call, it would probably manage its cash flows to prioritize interest payments on outstanding federal debt. That would leave less cash for other federal payments. The Bipartisan Policy Center has done a thorough analysis of the debt limit, the X date, and the impact of a default. In that analysis, they included estimates of Federal payments for June and July that could be endangered in the event of a default. Those payments would include Social Security, Medicare, federal civilian and military pay and retiree, veterans, and defense vendor obligations.

POTENTIAL BUDGET-DEBT DEAL

In recent history, Congress’s practice has been to lift the debt ceiling as part of other budget-related legislation. Since 2010, only 3 of the 10 laws that raised the debt limit were “clean” increases (limited to just raising the debt limit). Staff discussions on a budget deal that includes a debt limit increase are making progress, but a comparison of President’s Biden’s budget with the House-passed debt plan illustrates the sharp partisan budget differences that complicate getting negotiations.

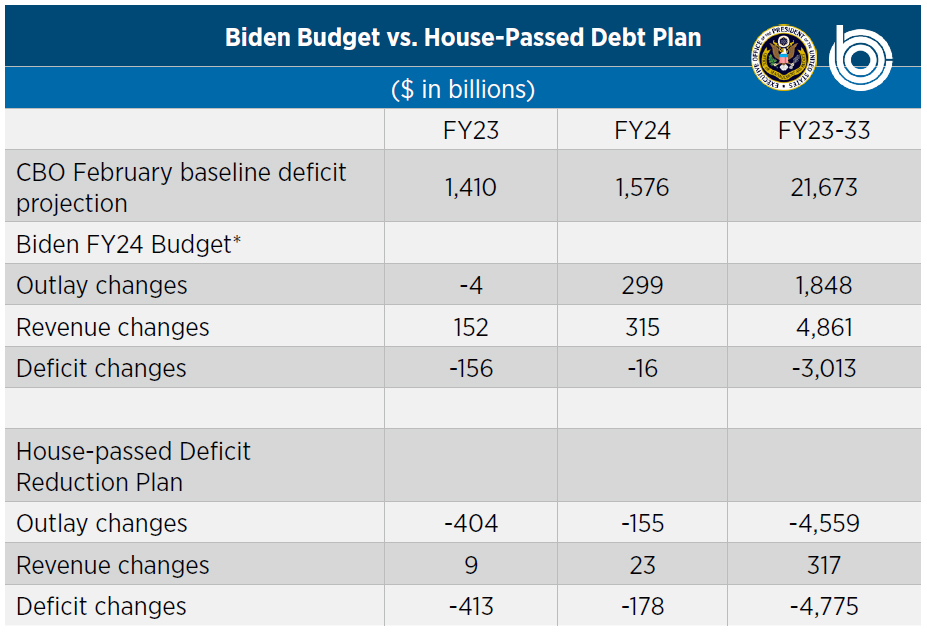

On March 9, President Biden submitted his FY24 Budget. According to the Office of Management and Budget (OMB), the President’s plan would reduce the deficit by $3 trillion for FY23-33. On April 26, the House passed HR 2811, the Limit, Save, and Grow Act of 2023, which according to the Congressional Budget Office would reduce deficits by $4.8 trillion for FY23-33. While each had trillions of dollars in deficit reduction, they took vastly different approaches.

As Chart I illustrates, the Biden budget increases spending by $1.8 trillion and more than offsets this increase by increasing revenues by $4.9 trillion. The House Republican debt legislation reduces spending by $4.5 trillion and increases revenues by repealing most of the green energy tax subsidies enacted in the Inflation Reduction Act.

*Estimates of Biden budget are from OMB, not CBO. All other estimates are from CBO. Chart I. Sources: Congressional Budget Office (CBO) and Office of Management and Budget (OMB).

Despite these differences, we think a combined budget deal and debt limit increase ultimately emerges. If the X date hits the first two weeks in June, a short-term debt limit extension may be needed to give negotiators time to finalize a deal and draft a bill, Congress to pass it, and get it to the President’s desk.

In terms of what a deal might look like, since 2011, there have been a series of bipartisan budget deals that set caps for two years, included other mandatory savings and suspended the debt ceiling. Based on past history, some of the President’s recent comments, and staff discussions to date, a possible framework on budget-debt deal follows:

- Debt limit suspension or increase through the 2024 election

- At least two years of caps on discretionary spending

- Rescission of unobligated COVID spending

- Tightening of work requirements for Food Stamps and Temporary Assistance for Needy Families (TANF) programs

- Permitting reform

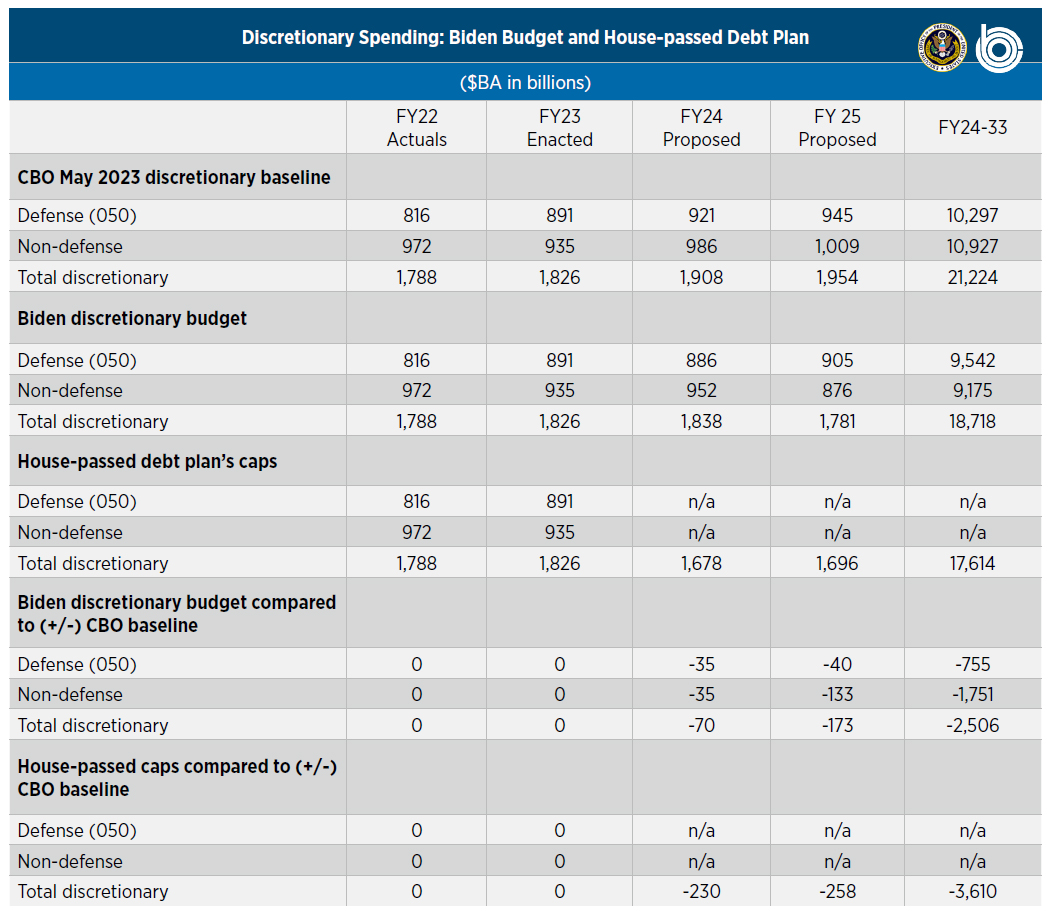

Getting agreement on each of the items will be a big lift. The differences on discretionary spending alone illustrate the challenge. While House Republicans have proposed major reductions in top-line discretionary spending, they want to increase defense spending. In the past, Democrats have insisted on rough “parity” for defense and non-defense. Despite these differences, eventually the President and Congress need to agree on a topline for discretionary spending. One possible outcome is that they agree to set caps on total discretionary spending and leave the defense and non-defense split to the appropriations process. Chart II compares the President Biden’s discretionary spending proposals and the discretionary caps proposed in the House-passed debt bill with the CBO’s February baseline. The House proposed annual caps on total discretionary spending for FY24-33. To simplify the display, the chart shows totals for that period.

The outcome of the White House May 16 meeting reduces prospects for a default. With a rapidly approaching deadline, stark policy differences between the two parties, the challenge of reaching a bipartisan agreement, vetting it, getting it drafted, approved in both Houses and sent to the President, mean the risk of a default cannot be completely eliminated.

n/a = not applicable. The House-passed bill only set caps on total discretionary spending. Chart II. Source: Congressional Budget Office.

FORECAST

95% a bipartisan budget-debt deal is reached, possibly necessitating a short-term debt limit extension if the X date arrives in early June.

FORECAST

65% a two-step process that includes a short-term debt limit extension is needed.

FORECAST

5% Treasury defaults.